Definitions

A bridge loan is any loan with a duration of 36 months or less utilizing interest-only payments for the duration of the term and containing a balloon payment at the end of the loan. Bridge loans are commonly referred to as residential transition loans (RTL), fix-and-flip, non-owner occupied, hard money, or in other terms that describe a short-term loan generally secured by a residential property for investment purposes.

DSCR loans are 30-year term loans secured by rental properties. DSCR stands for Debt Service Coverage Ratio, which identifies that the primary underwriting for these loans is done by dividing the monthly net operating income of the property by the monthly debt service.

A User refers to a unique company using the Lightning Docs platform. If multiple individuals within the same company access the platform, they are collectively counted as a single user.

Methodology

Loans below $50,000 and above $5,000,000 have been removed from the data set.

Loans with interest rates below 4% and above 20% have been removed from the data set.

For the loan volume slides, the user must have signed up with Lightning Docs prior to 2025.

I often write about the macroeconomic factors that create noise in our industry—and how the most successful lenders block it out and stay focused on what they can control. In April, however, that “noise” became impossible to ignore.

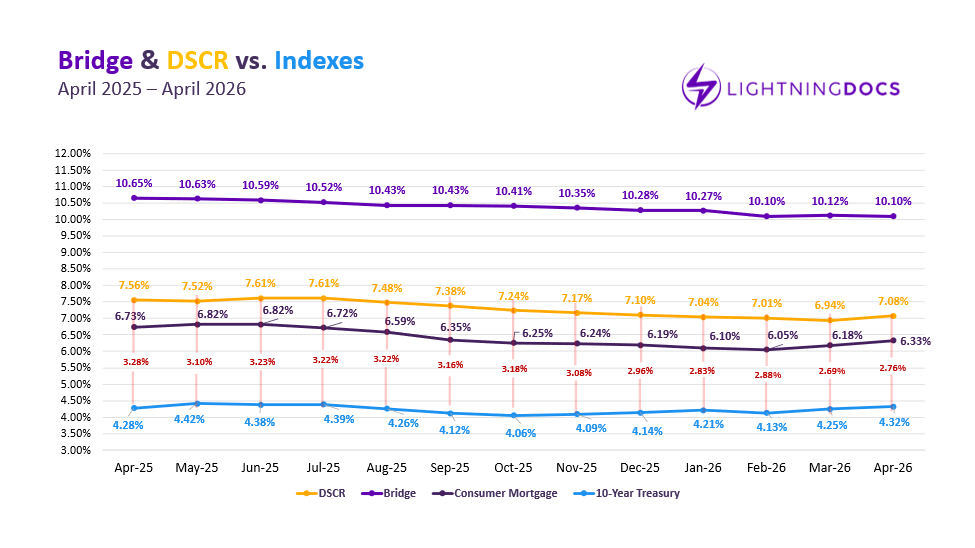

As the war with Iran continued and oil prices remained elevated, the 10-year Treasury yield climbed again—marking its sixth increase in the past seven months. That shift put an end to the steady decline in DSCR interest rates, while bridge loan rates have held relatively flat since February of this year.

Here’s how that shift played out across private lending in April.

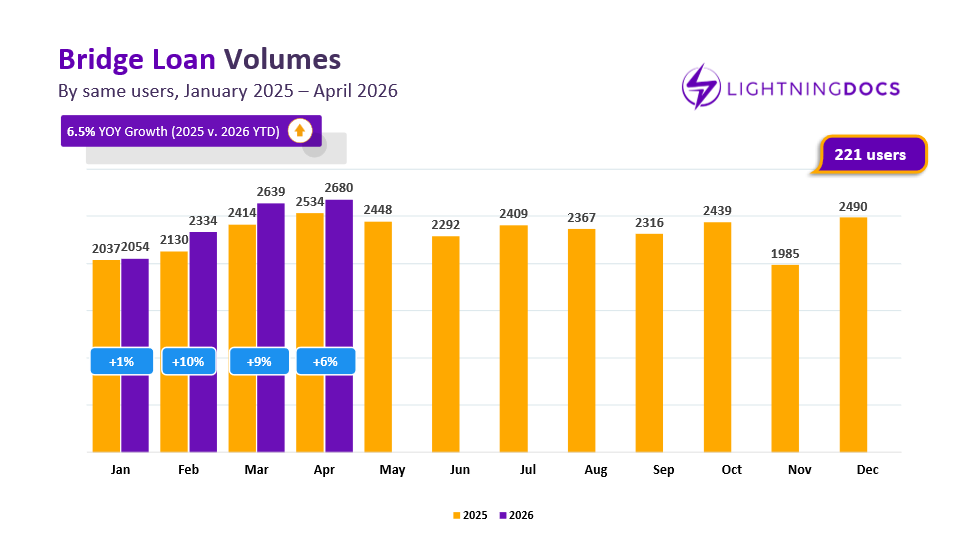

Bridge Loan Volumes

Bridge loans continue to present a mixed outlook. On one hand, the 2,680 loans produced by users with us since the start of 2025 represent just a 6% year-over-year increase—modest growth by historical standards. On the other hand, that same volume marks a record high on Lightning Docs for the second consecutive month.

Despite ongoing headwinds for short-term lending, private lenders have remained resilient and continue to push volumes higher, albeit at a slower pace.

Bridge Loan Interest Rates and Average Loan Amounts

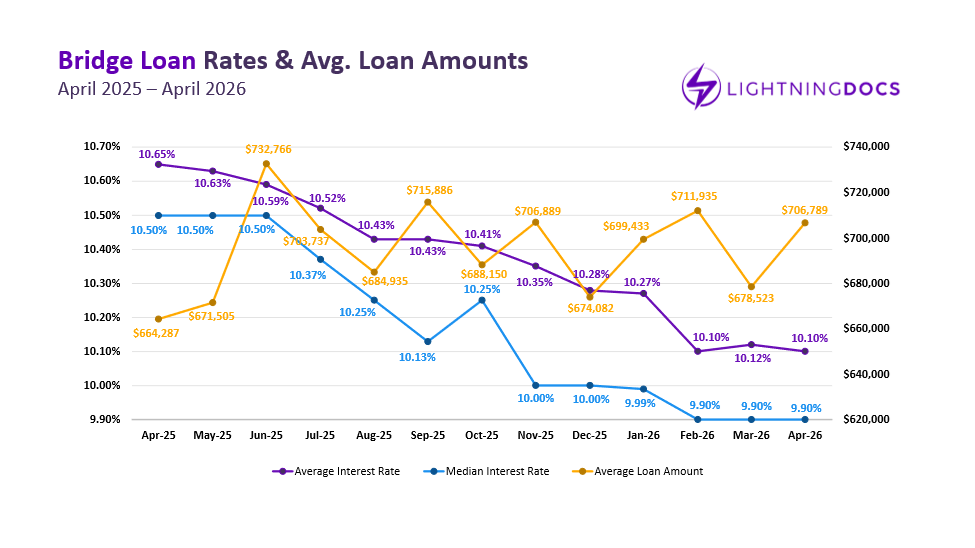

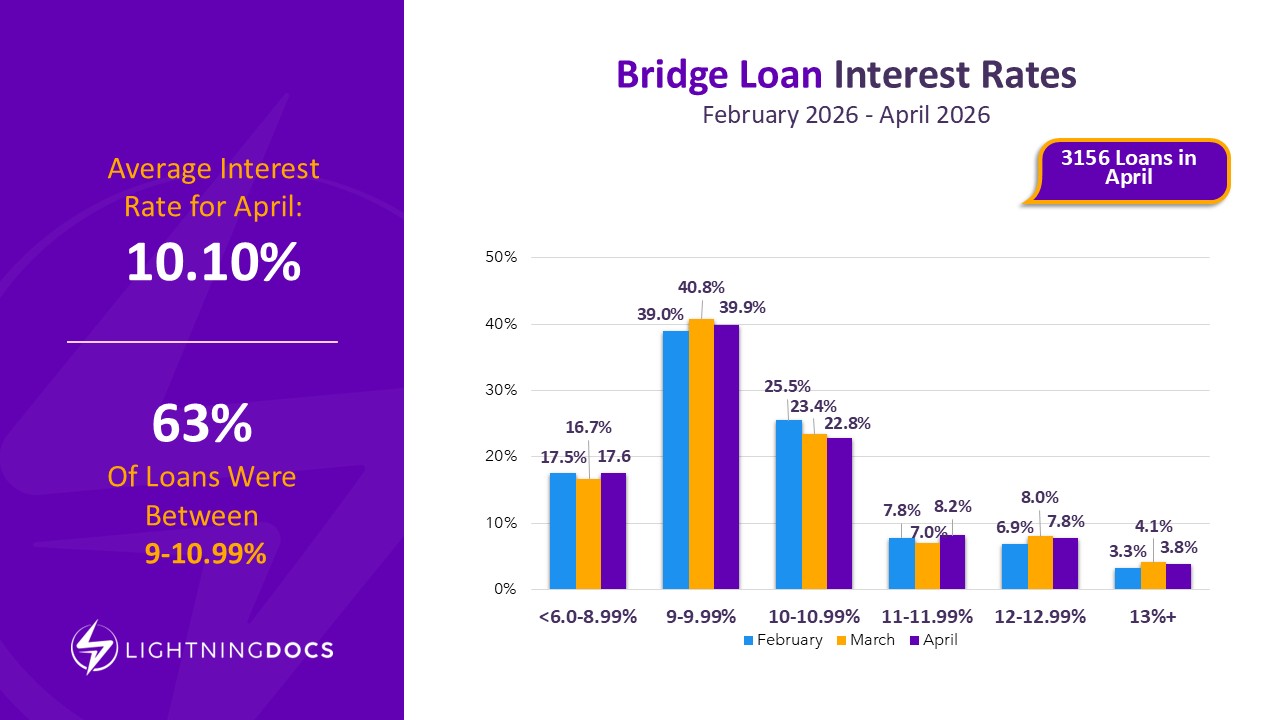

As noted at the start of this report, bridge loan interest rates remained largely unchanged, declining by just two basis points month-over-month. Average loan amounts moved up to $706,789, but have remained within the same range for almost a year. Interestingly, almost 40% of the 3,156 bridge loans produced in April had interest rates between 9-9.99%, demonstrating a flight to safety and steep competition.

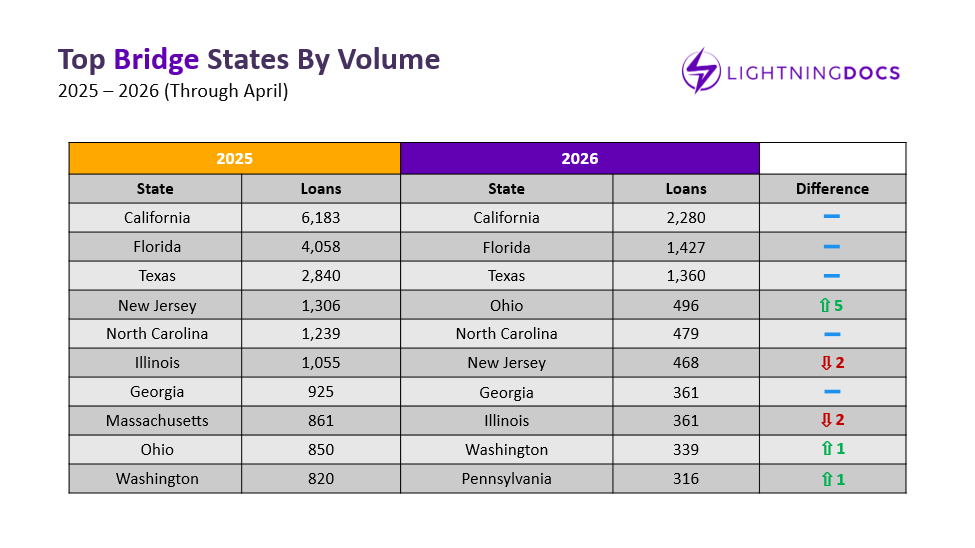

Top States for Bridge Loans

There was minimal movement among the top states for bridge loans in April. The most notable trend this year remains Ohio’s rise to the number four spot. Outside the top 10, Massachusetts (#12) and Oregon (#15) continue to gain momentum, with transaction volumes increasing each month in 2025.

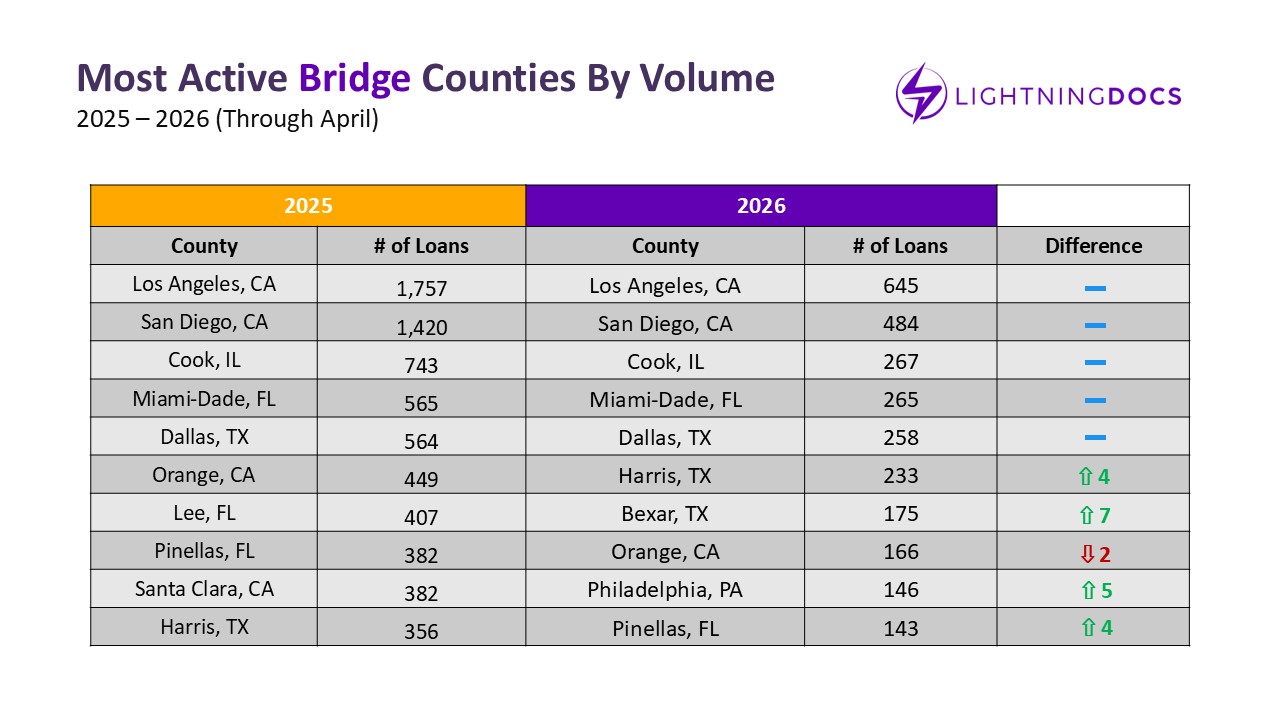

Top Counties for Bridge Loans

A strong April from Philadelphia, PA, and Pinellas, FL (St. Petersburg) pushed both back into the top 10, displacing Santa Clara, CA, and Lee, FL (Cape Coral). In fact, from March-April, Philadelphia more than doubled the number of transactions it did from January-February. Outside the top 10, King County, WA (Seattle) and Maricopa County, AZ (Phoenix) have steadily increased volume each month this year, each posting top-10-level production in April.

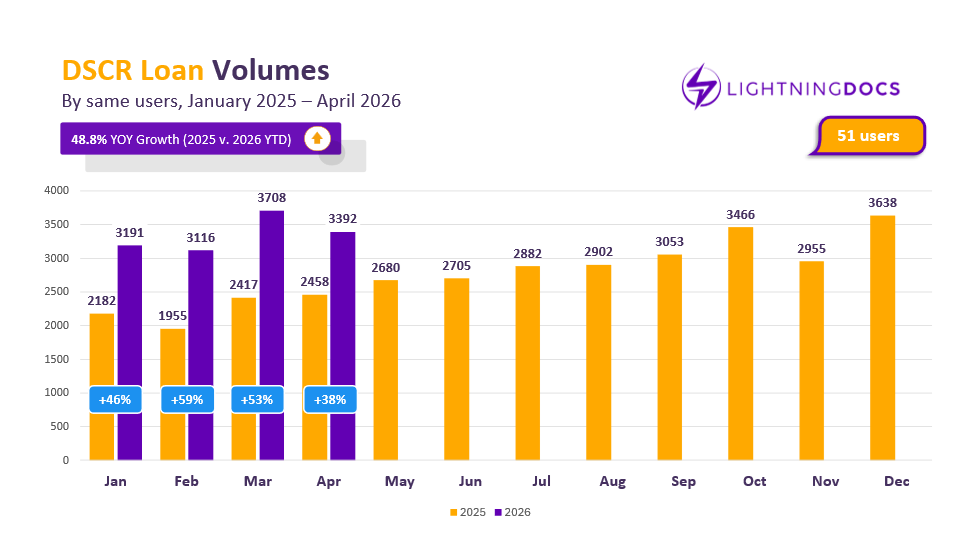

DSCR Loan Volumes

DSCR loan transactions among users with us since the start of 2025 are up 38% year over year. However, that growth is no longer linear. After a prolonged period of steady monthly increases, transaction volume has begun to fluctuate. April’s 3,392 DSCR loans is slightly lower than levels seen six months ago in October.

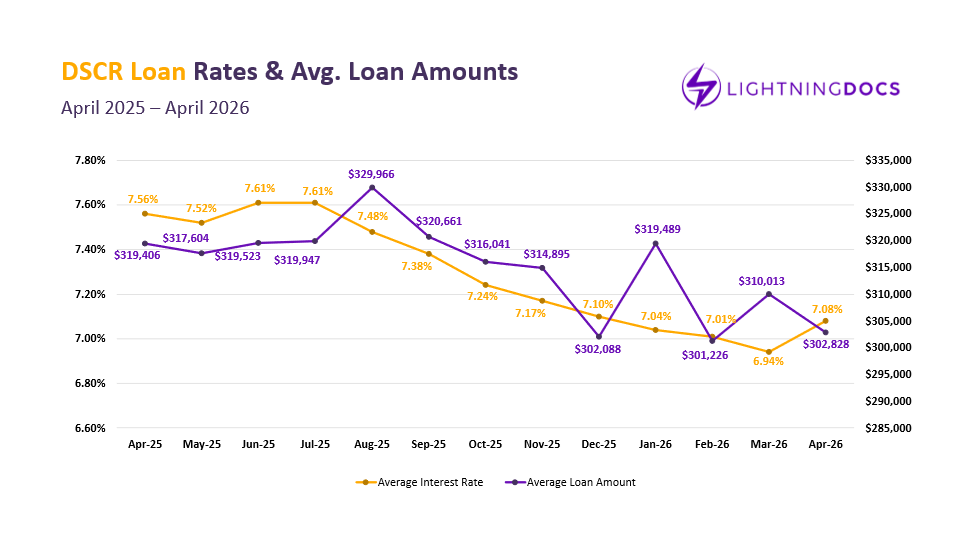

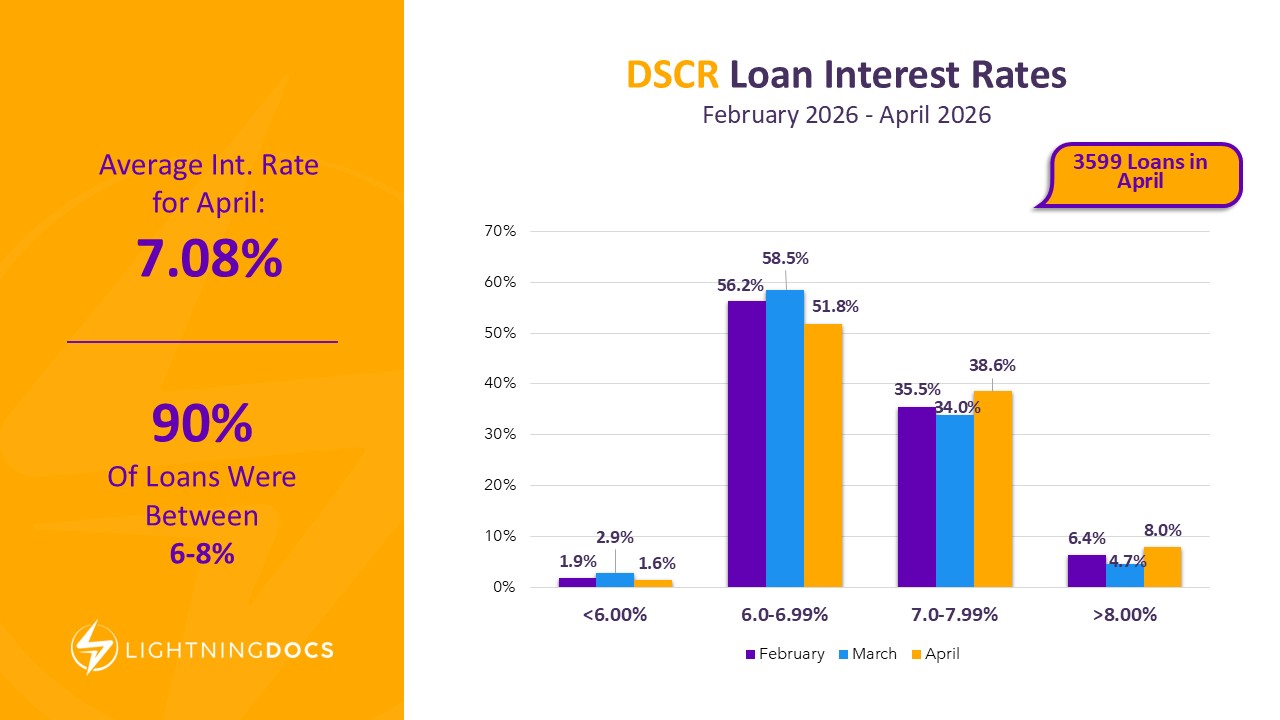

DSCR Interest Rates and Loan Amounts

The primary driver of April’s pullback in DSCR volume is clear: interest rates.

After briefly dipping below 7% in March, DSCR rates rose sharply to 7.08% in April—a 14 basis point increase and the largest monthly jump since late 2024.

That shift is reflected across rate distribution. Loans in the 6.00–6.99% range declined by nearly 7%, while loans above 8% nearly doubled, now accounting for 8% of all DSCR originations. Meanwhile, sub-6% loans—once an emerging segment—fell to just 1.6% of total volume.

Bridge and DSCR vs Benchmark Indices

As highlighted earlier, macroeconomic conditions are now directly influencing private lending activity. Nowhere is that more evident than in the 14-basis point increase in DSCR rates during April, driven in part by a 29-basis point rise in the 10-year Treasury yield from February through April. Encouragingly, spreads remain relatively tight at 2.76%.

Bridge loan rates declined slightly by two basis points in April, while consumer mortgage rates moved higher, reaching 6.33%—their highest level since September of last year.

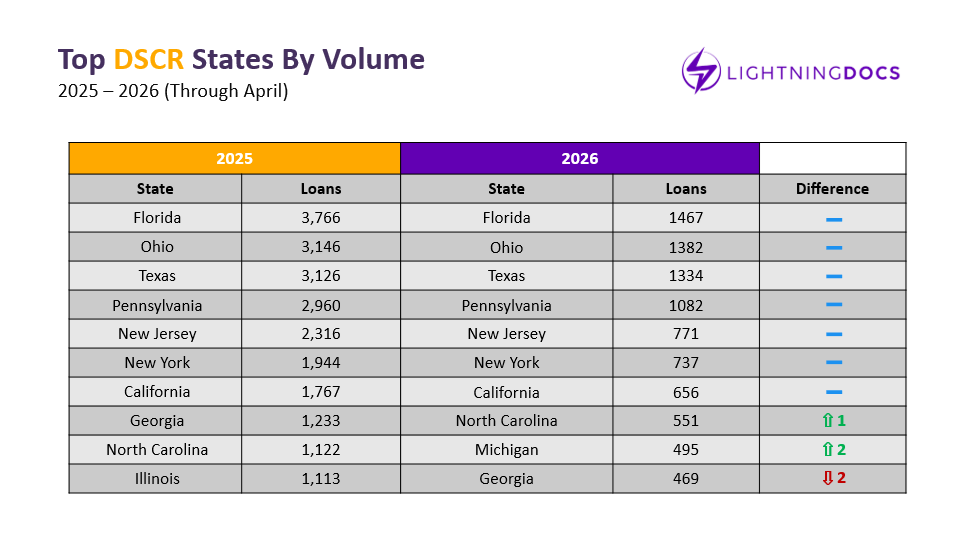

Top States for DSCR Loans

The top states for DSCR loans remain largely consistent month to month. The only change in April’s top 10 was Georgia replacing Maryland at the number 10 spot.

After a strong start to the year, Maryland slipped to 13th, with Missouri and Illinois both surpassing it following strong April performance.

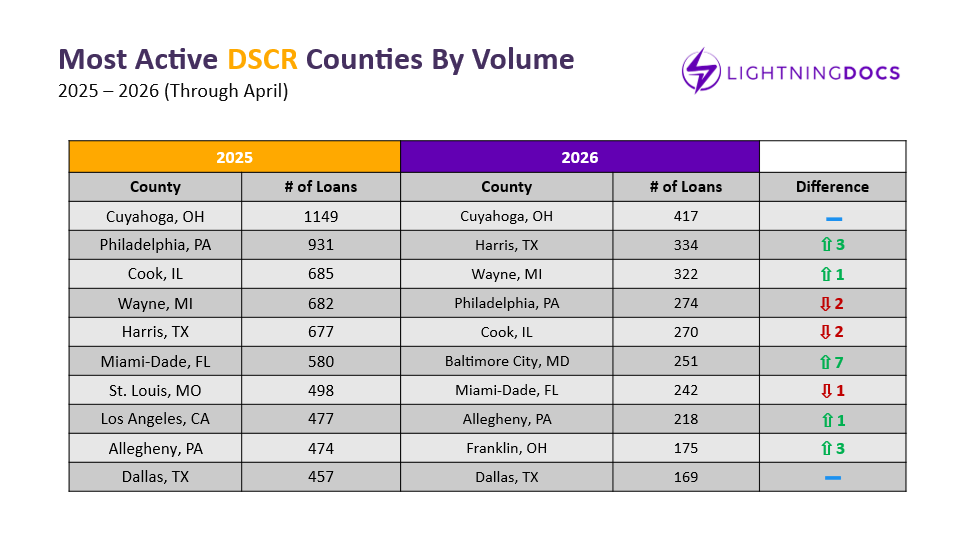

Top Counties for DSCR Loans

Top DSCR counties also remained relatively stable. Philadelphia, PA and Cook, IL rebounded after slower starts to the year and are now climbing back up the rankings.

Meanwhile, Baltimore City, Miami-Dade, Allegheny, PA (Pittsburgh), and Franklin, OH (Columbus) each recorded their lowest DSCR output of the year.

Just outside the top 10, Jackson County, MO (Kansas City) continues to stand out as volume has increased each month in 2026, with the county posting the sixth-highest total of any market in April.

April introduced a turning point for private lending. Rising Treasury yields halted the steady decline in DSCR rates and began to weigh on transaction consistency.

Bridge lending continues to push forward, reaching new volume highs despite slower growth. DSCR lending, however, is showing early signs of sensitivity to rate increases, with volume flattening and pricing shifting upward.

The data points to a more balanced and rate-driven environment ahead.